Speer: What IF We Did Nothing?

“One of the greatest pains to human nature is the pain of a new idea…after all, your favorite notions may be wrong, your firmest beliefs ill-founded.” - Walter Bagehot

R-CALF’s recent press release reminded me of one of those Seinfeld episodes where someone gets labeled. You know, low-talker, close-talker, double dipper, antidentite. R-CALF lumps everyone together as “beef packers and allies” if you don’t align with their thinking.

The column then invokes a subsequent label: “the ostensibly lone wolf cheerleader… Nevil Speer…” Intrigue and innuendo are an interesting twist to any plot. But Mr. Bullard has zero knowledge (we’ve never even spoken) to make any sort of claim regarding the foundation of my work. Label me however you want, but rest assured, there’s nothing “ostensible” about any of it.

None of that really matters. What’s more important are the issues at hand. That is, what industry problem are we trying to solve? For R-CALF the crux of it goes something like this:

- packer bad,

- market unfair,

- cattle too cheap,

- producer unprofitable.

And the degree to which these occur is in direct proportion to the thinning of the cash market.

For now, though, let’s get off the cash trade / market merry-go-round. Rather, let’s focus on B-thru-D, above. After all, your banker doesn’t really care about prices, the overriding concern is profit – business first, market second.

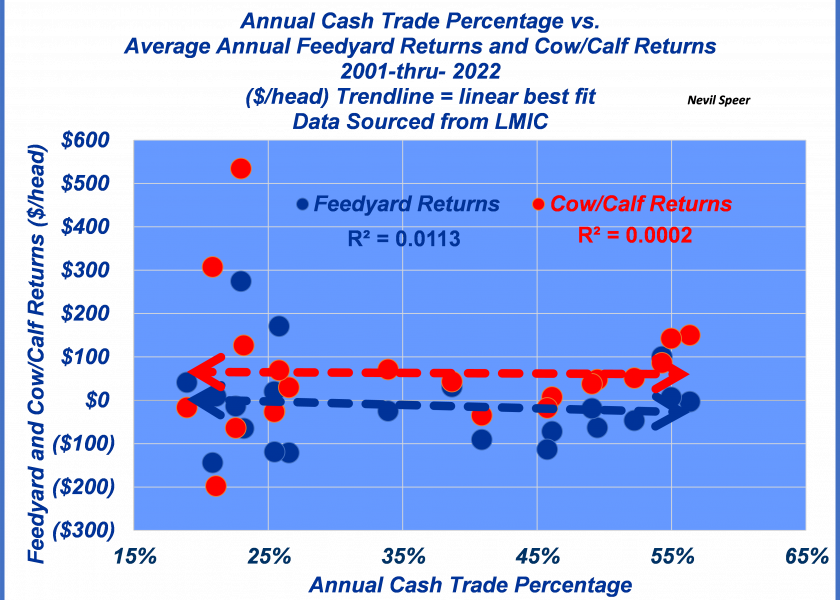

To that end, the attached graph highlights the relationship between cash trade and annual returns for feedyards and cow/calf operations, respectively. Twenty-two years of data sourced from LMIC tell a compelling story (or lack thereof). In both instances, the regression line is flat; there’s no relationship between cash trade and returns for feedyards or cow/calf operations. Simply put, there’s no connection between B and C and D above.

Now, let’s take a broader, aggregate view at how this plays out from an industry perspective. Recall the beef industry sold off nearly 3.75 M cows between 2007 and 2014. But what came next? Producers went right back to work and turned from sellers to investors. The cowherd rebounded by nearly 2.75 M head in the next five years (and all the while the level of cash trade was diving to new lows). Cattle feeders are on the frontlines of all this but they, too, remain busy. This year’s starting feedlot inventory is the largest since 2008 (all that while the cash market has been shrinking).

The most important shift of all, during the past twenty years, has occurred on the consumer front. Beef has differentiated itself in the marketplace. As a result, beef spending has outpaced the competition. Despite R-CALF’s claims to the contrary, that’s meant better prices at the farm gate. For example, between ’00 and ’09 a 550-lb steer averaged ~$600/head; the next ten years saw that value jump to $970/head! And what’s more, producers now have access to go even further with more value-added opportunities than ever.

Circling back to the question at hand: what industry problem are we trying to solve? Given the facts (stubborn things), R-CALF’s conjecture about “beef packers and allies” seems to be a show about nothing. And in response, what if we did nothing? Because if it ain’t broke, don’t fix it – especially if it means avoiding government intrusion.

Nevil Speer is based in Bowling Green, KY and serves as Director of Industry Relations for Where Food Comes From (WFCF). The views and opinions expressed herein do not necessarily reflect those of WFCF or its shareholders. He can be reached at nspeer@wherefoodcomesfrom.com.