Speer: Chessboard of Producers

My previous column surrounded a recent press release featuring USDA ARMS (Agricultural Resource Management Survey) cow/calf return data. The press release argued returns in recent years indicate producers have a need to “…fix your industry’s broken market.” And ultimately government needs to step in; a subsequent press release on the topic declared: “We must fix this with legislation.”

However, as noted in my column, the “…USDA data tells a positive (not negative) story…That’s directly attributable to better demand and stronger spending over time…” Therefore, any call for some legislative “fix” requires a deeper look into how that plays out in the business (lest something really gets broken along the way).

Given that, it’s valuable to provide some overview of the cow/calf sector (relying on USDA data). We’ll start at the top and drill our way down

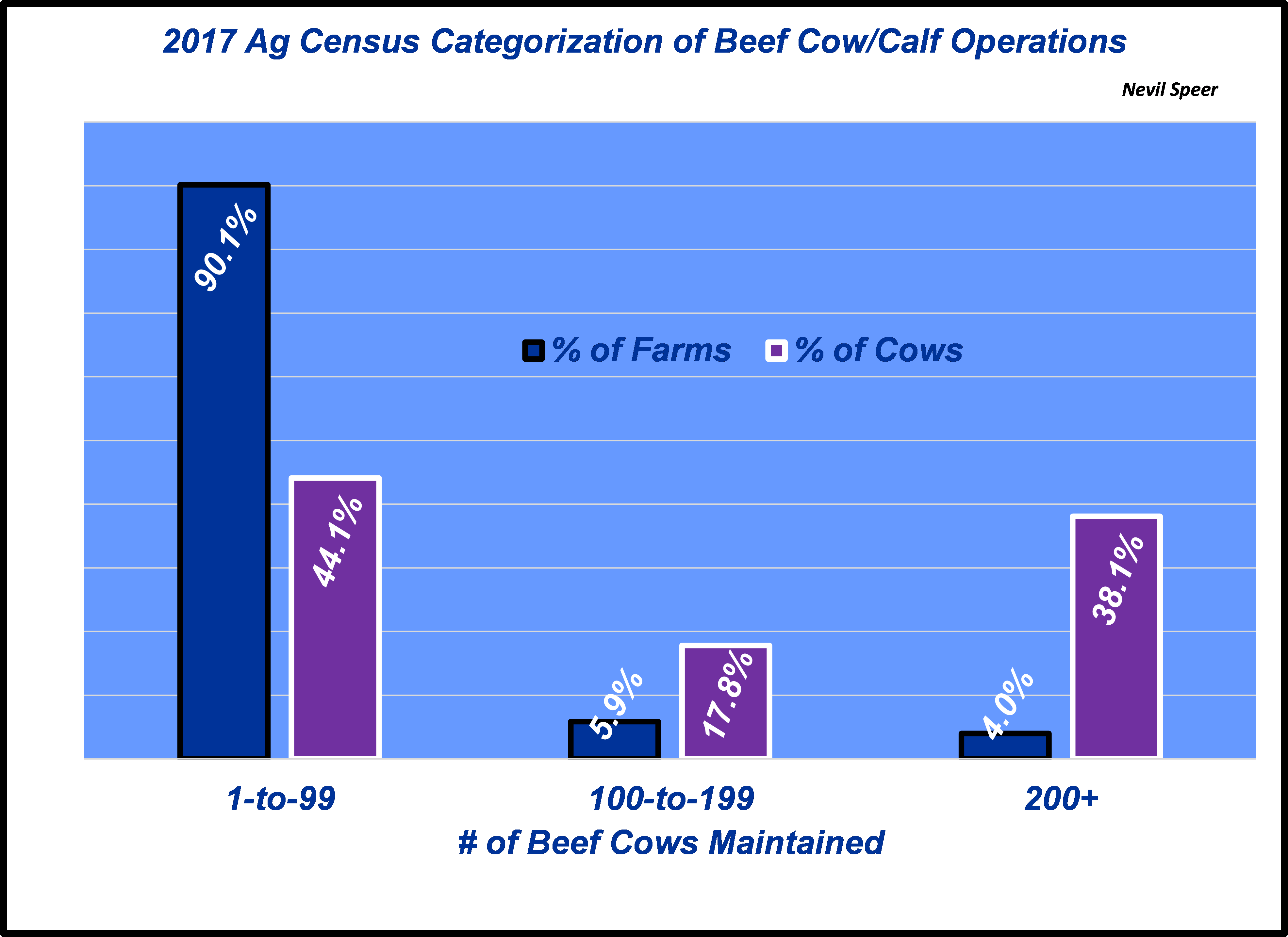

Ag Census: The 2017 census counted roughly 729,000 beef cow operations running approximately 31.7M cows. The overwhelming majority of operations (96%) manage less than 200 cows. However, those operations with 200-or-more cows (4% of all operations) manage nearly 38% of the nation’s cow inventory (12.1M head) – right in line with the ’07 and ’12 Census data. (see first graph)

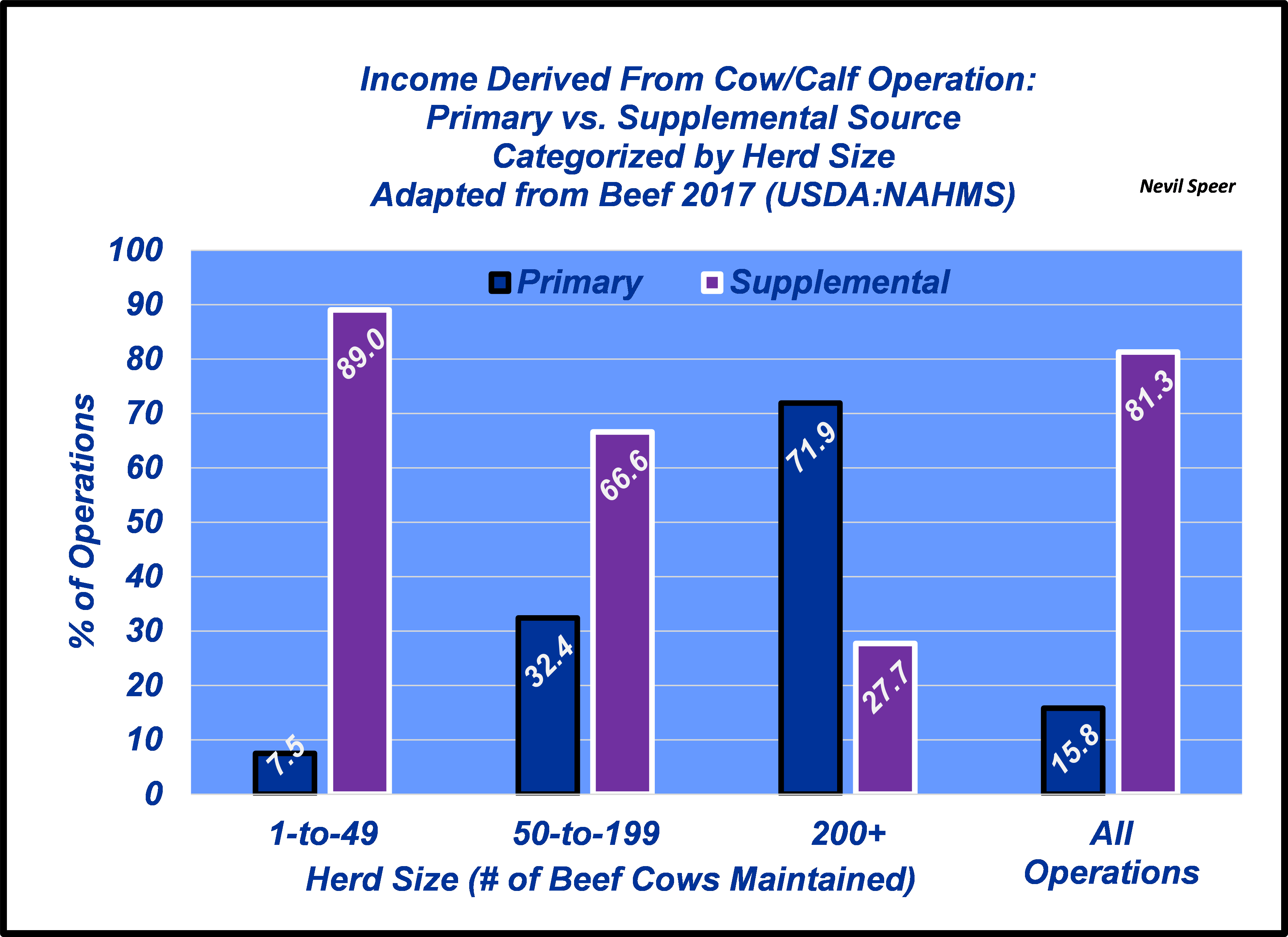

Beef 2017: USDA’s National Animal Health Monitoring System Beef 2017 survey provides an extensive and comprehensive overview of management practices within the cow/calf sector. Most significant here, the survey categorizes income (primary vs. secondary).

The bulk of owners with less-than-50 cows do NOT consider the operation a primary source of income. And the 200+ cow operations? Even then, only 72% consider the enterprise to be a primary income source. (see second graph)

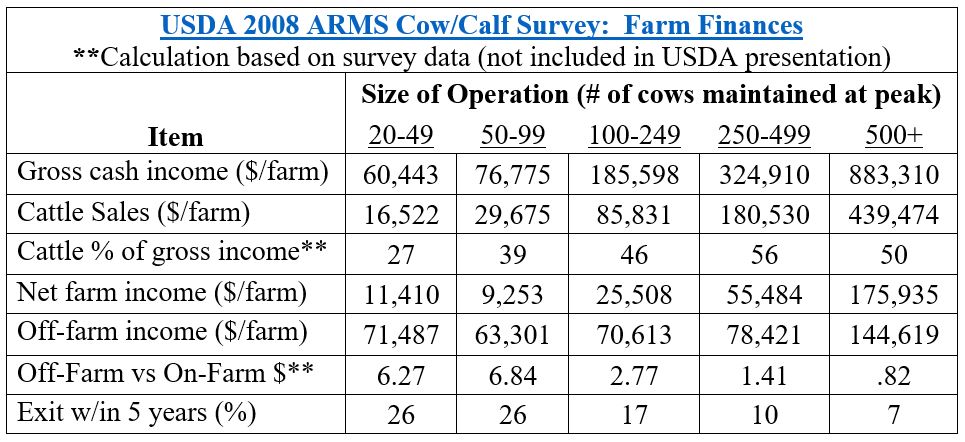

ARMS: Finally, there’s the ARMS survey data cited at the start (see: 1. ’82-to-’89, 2.) ’90-to-’95, and 3.) ’96-to-’21). USDA summarizes a variety of survey questions that provides a more granular look into the sector. With respect to farm finances, several of the more significant items are highlighted in the table below.

In particular, note the following:

- Cattle sales as a percentage of total farm income peak in the 250-499 cow category. But that still represents less than 60% of total income. That lines up with the NAHMS data cited above – however you cut it, in most instances, cows are NOT the primary source of farm income.

- Off-farm income represents a variety of sources including employment and/or alternative business ventures. Not surprisingly, smaller cow herds are more heavily dependent on off-farm income. However, even larger operations still find ways to generate significant income separate from the farm.

- Perhaps most important, the number of producers with less-than-100 cows indicate their intent to exit the business within five years is nearly 4X versus those operations 500+ cows. Accordingly, those 100-or-fewer-cow operations are less committed to the business over time and more likely to enter-and-exit depending on any number of variables.

USDA summarizes the survey with the following observation: “Most beef cow-calf production occurs on large farms, but cow-calf production is not the primary enterprise on many of these farms. Findings suggest that operators of beef cow-calf farms have a diverse set of goals for the cattle enterprise.” (emphasis mine)

Chessboard of producers: Given that summary of the business, Adam Smith’s wisdom is particularly fitting. His description of economic activity being: “…great chess–board…” in which “…every single piece has a principle of motion of its own…” But Smith’s next observation is even more significant; the motion is “…altogether different from that which the legislature might choose to impress upon it.”

Any proposal to “fix” the business is inherently paradoxical. After all, the business is particularly complex and legislators generally aren’t very good chess players (see Knowledge Problem) – they can’t see the game beyond one or two moves. The best “fix” is to do nothing – and enable cow/calf producers to enjoy the full benefits of a free market.

Nevil Speer is an independent consultant based in Bowling Green, KY. The views and opinions expressed herein do not reflect, nor are associated with in any manner, any client or business relationship. He can be reached at nevil.speer@turkeytrack.biz.