After a mostly sluggish April, market-ready fed cattle saw a solid rally in the North and steady money in the South. Futures markets began to look past the psychologically bearish H5N1 virus news.

A snowballing effect from several factors has led to the present market flush in cattle futures and provides a stark contrast between emotion and factfulness.

Reported national feeder cattle volumes (auction, direct and video/internet) are up 5.6% year-over-year since Labor Day, with the majority in September which contributed to the large September feedlot placements.

Cash fed cattle prices have increased 4.8% during the month of November in the past five years, yet carcass cutout values have begun the month in a bit of defensive pattern.

Last week saw several feedyards pass on steady bids from packers. Cattle feeders are counting on declining numbers of Choice carcasses to bring packers back with higher bids.

Beef demand has been remarkably robust through many shocks in recent years and continues to surprise and impress despite the nervousness of the industry to the challenges facing consumers.

Cash trade was light as many cattle feeders passed on steady bids. Feeder cattle and calves traded mixed. Live and feeder futures contracts posted weekly gains.

Cattle prices were weaker on the week with volatility in the futures markets and the season's first cold spell on the way. Wholesale beef prices traded higher seasonally.

USDA's recent October 1, 2023, Cattle on Feed report offered a few surprising numbers. How does that report square up with previously released USDA data?

Packers were forced to add to their inventory and pushed prices $2 higher last week. The surprises in the Cattle on Feed report may offer a reason to push prices lower, yet feedyards maintain the upper hand.

Cattle feeders saw $1 to $2 gains in all regions during the week, but a struggling futures market and an unfriendly placement number in Friday's Cattle on Feed report may drag on cash prices in the short-term.

For cow-calf producers, fall is often a time for preconditioning, weaning and marketing calves. While prices will likely be towards the top end this year, could you still be leaving money on the table?

With cattle prices strong, serious inventory issues continue as the USDA is set to release the newest cattle on feed report on Oct. 20. Here's what experts are saying about the upcoming report and herd expansion.

Ground beef is the inexpensive alternative consumers turn to when prices rise. However, the overall decline in beef production means that ground beef supplies will be smaller and prices higher going forward.

For cattle producers across the U.S., a number of factors make the idea of herd rebuilding a bit less enticing. Experts share why the U.S. cowherd is not on the fast-track to recovery.

Although August exports of U.S. pork were steady year-over-year, beef exports were well below the large totals of August 2022, USMEF reports. Pork exports were led by Mexico and beef exports showed improvement over July.

Outside factors pressured cattle markets through most of the past week before futures and wholesale beef prices rebounded on Friday. Market fundamentals remain positive for cattle going forward.

Fall calf runs typically mean auction volumes increase and prices decrease to seasonal lows. This year is quite different with feeder cattle and calf prices sharply higher than one year ago while volumes are much lower.

The latest Cattle on Feed report puts inventories down 2.2% from last year, and up slightly from the August summer low, which was the lowest monthly on-feed total since September 2019.

America’s shrinking cow herd has generated sharp packer interest for the smaller pool of cows aggressively culled in drought regions leading to record high cutter cow carcass values.

Live cattle trade is part of the integrated markets for beef and cattle in North America. Canada and Mexico account for 100 percent of U.S. cattle imports and 95 percent of cattle exports.

Cattle inventories simply are not large enough for the packer to build any market leverage. Reluctantly, packers bought cattle at steady to higher money and cowboys will seek more this week.

Cash cattle trade was sluggish as feeders and packers dig in their heels. Feeder cattle and calf prices continue marching higher even as drought sends some early-weaned calves to market.

U.S. pork exports wrapped up an excellent first half of 2023 with another strong performance in June. Although numbers are below the record pace established in 2022, June beef exports topped $900 million in value.

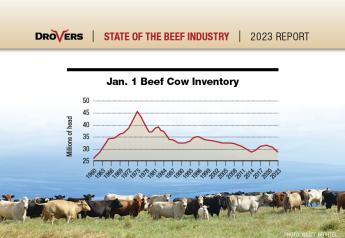

The most recent USDA cattle inventory reports reveal herd numbers continue to shrink, the 2023 mid-year beef cow inventory the lowest in the data set dating back to 1973. Feeder supplies will likely shrink through 2024.

Cattle feeders held firm to higher asking prices and packers continued to wave lower bids with only a few cattle trading hands. Leverage remains in the feeder’s hand as packers must begin filling Labor Day orders soon.

Packers and cattle feeders spent the week in a standoff ahead of USDA's dual July reports that were bullish as expected, suggesting a 3% decline in cattle inventories and a 2% decline in cattle on feed inventories.

Disciplined hedgers protect themselves against noise and volatility – the very essence of why futures markets exist, and why smart feeders use that tool.

Beef imports will continue to be supported by higher domestic beef prices and the reduction in U.S. processing beef supplies due to reduced cow slaughter.

Wholesale beef prices continue to support packer margins even as negotiated cash cattle trade well-above the five-year average. Pork producers enjoy a market rally that has lifted margins out of the red.

Many similarities exist between today's cattle market and that of a decade ago. But this year’s market is not, as Yogi Berra once said, “déjà vu all over again.”

The current high cattle prices were not a matter of “if” but “when,” following severe drought across cattle country. However, in volatile markets, should cow-calf producers be optimistic about profits in 2023?

Packers were aggressive bidders in all regions as cash fed cattle markets made historic late-season moves higher in the holiday-shortened trading week.

Increasingly tight cattle supplies suggest that margins at all levels above the cow-calf sector will be squeezed in the coming months. The severity of the squeeze and the timing will vary across beef industry segments.

Wholesale beef prices hit a recent low the end of March at $280.51 per cwt., but the steady march higher since then put Friday’s close as the highest Choice cutout value for that week on data available back to 2004.

Passing on bids at record levels was common early last week and negotiated sales printed new record highs for the third week in a row. Analysts and cowboys are eyeing additional gains next week.

Given growing expectations that drought conditions will moderate through the coming months, bred cow and heifer values are likely to increase sharply by this fall.

Over the past four weeks beef production has averaged 6.4% lower than last year. Production is expected to drop more sharply the remainder of the year.

Instability in equity markets proved a drag on futures last week, providing an incentive for feeders to trade on lower bids. Packers will continue to struggle with inventory going forward.

The positive basis created by weaker futures prices enticed hedged feeders to accept lower bids early in week. Friday's cattle on feed report further confirms a shrinking supply and will lend price support.

Cash fed cattle traded at steady money in all areas after futures markets moved lower Friday. Feeder cattle and calves posted significant weekly gains.