Speer: Farmers’ Share An Iffy Indicator

Dr. Scott Sagan (Stanford University) is credited with remarking that, “Things that have never happened before happen all the time.” For the beef industry that reality began three years ago with the fire at Tyson’s Holcomb facility; then came Covid; and now, drought.

All the while there’s been lots of brouhaha related to cash trade. The argument being record large packer margins must mean the “market is broken”. More pertinent here, it’s also led to focus on beef price spreads in general.

Famer’s share, the percentage of the retail dollar captured at the farmgate (i.e. the cattle feeder), is an important topic. However, it’s easily misinterpreted and often conflated with other issues. As such, it’s worthy of some detailed discussion (and requires more than a single column).

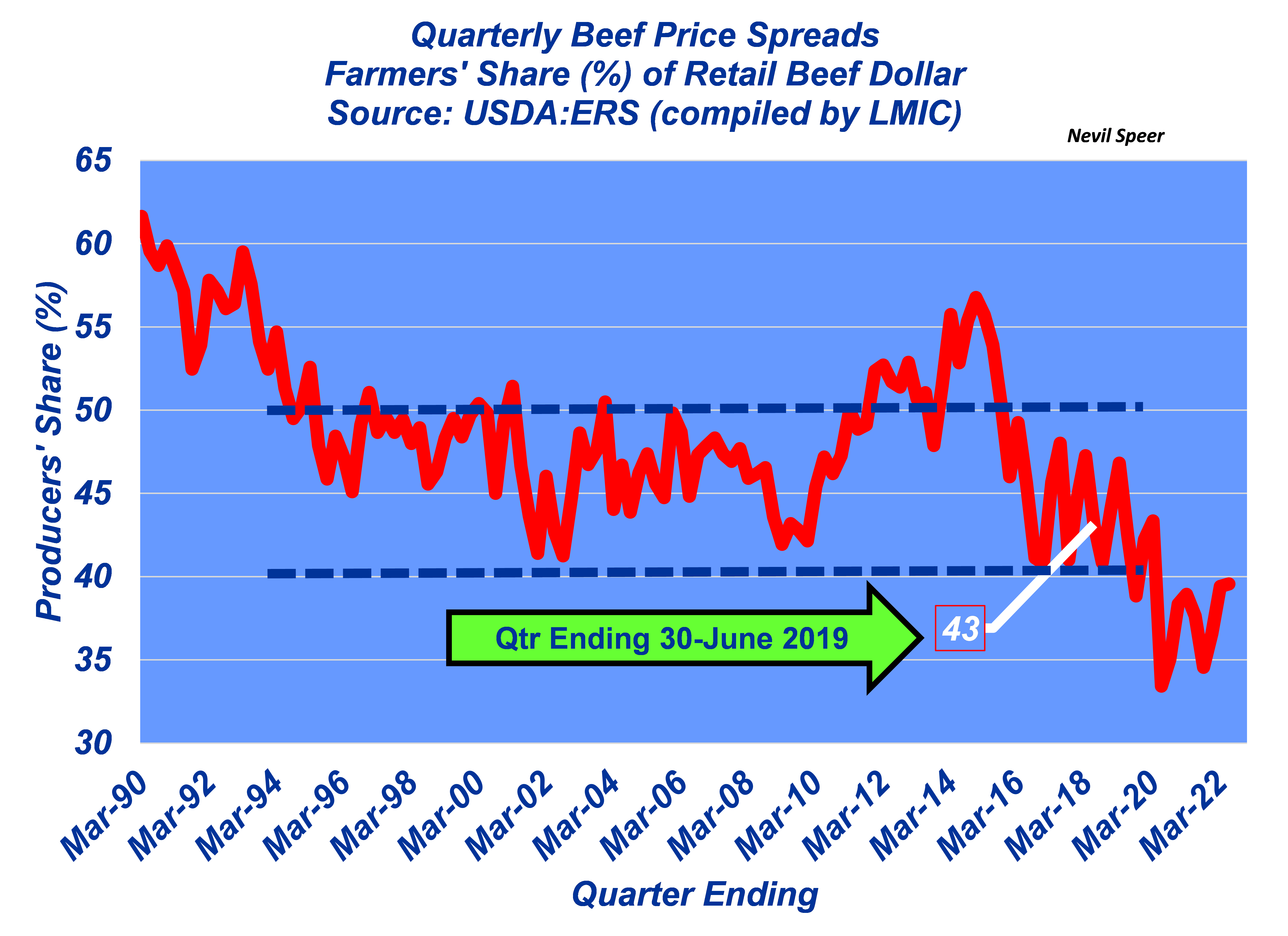

The first graph provides some longer run perspective. Note the measure largely fluctuated between 40-to-50% from the mid-90s all the way through the second quarter of 2019 – just prior to the Tyson fire (highlighted on the graph). In other words, the recent break is a near-term phenomenon. Note also, the measure has recovered from its lows as business is normalizing.

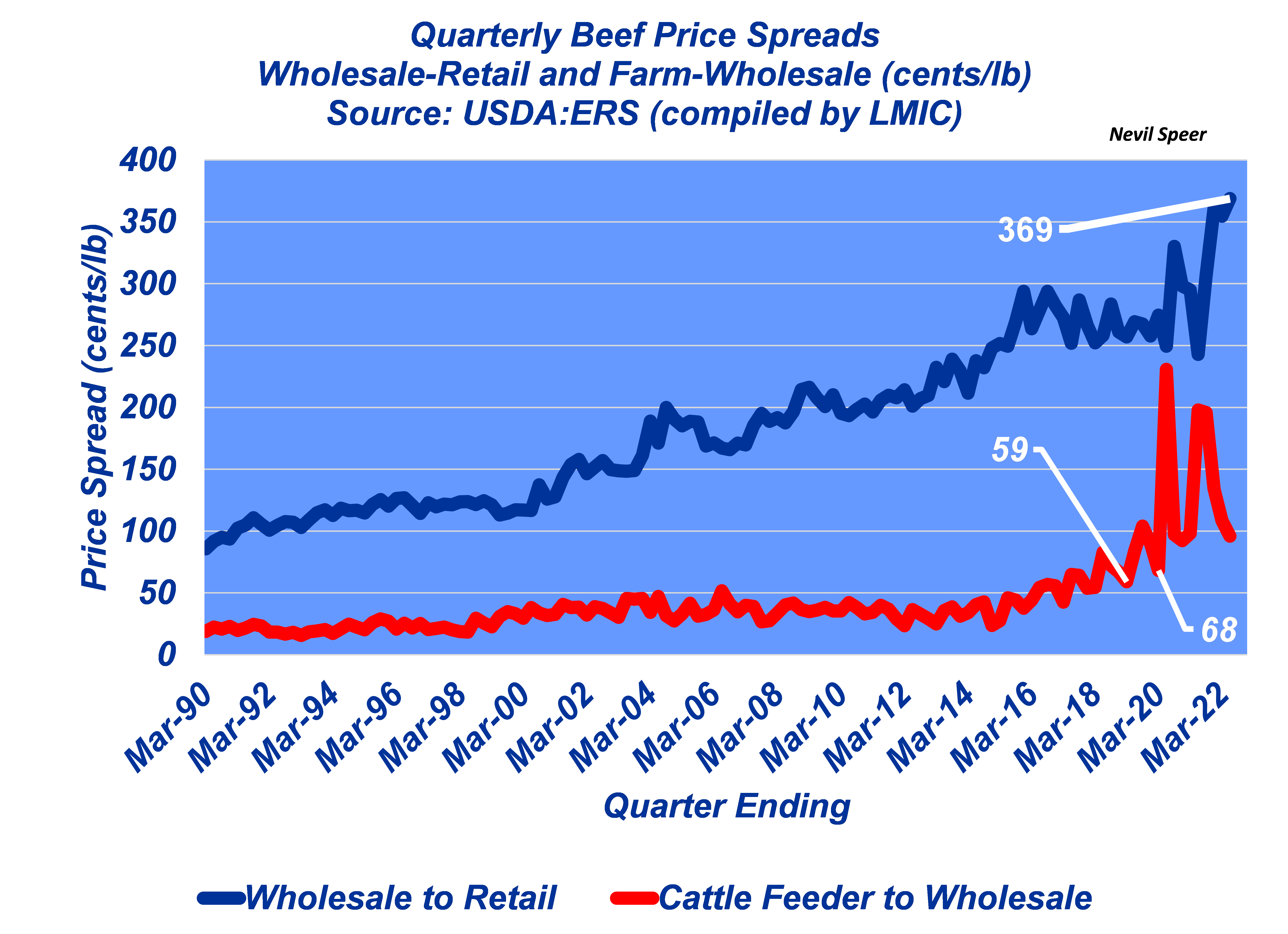

Meanwhile, it’s also important to point out farmers’ share is a function of two separate price spreads: 1) cattle feeder-to-wholesale and 2) wholesale-to-retail, respectively. The second graph details the individual components.

The cattle feeder-to-wholesale spread surged following the Tyson fire and subsequently settled back to 68 cents/lb just prior to Covid (compared to 59 cents/lb the year prior). It then surged to $2.49/lb and is now moderating into the second half of 2022. Meanwhile, the wholesale-to-retail price spread just marked an all-time high ending the second quarter at $3.69/lb. With that in mind, there’s a couple of broader points that require emphasis.

First, the measure misses some of the market’s realities. Namely, the reporting of farmer share is dependent on USDA (ERS) simple average retail prices – NOT realized volume-adjusted retail prices. The actual retail price paid by consumers is lower than the price utilized by USDA due to the ever-growing number of retail features and promotions to drive store traffic. As a result, producer share is inherently understated over time. (For more on this, see work of Dr. Glynn Tonsor, Beef Industry Outlook, 2018).

Second, while it sounds meaningful, farmers’ share is not a very good measure of industry viability. Brester et al. (2009), in their seminal paper on the topic, observe that: “The lack of informational content in [farmer share] statistics suggests these data should not be used for policy purposes.” Most notably, investment by processors and/or retailers to increase demand will inherently reduce farmers’ share yet make the industry (including producers) better off over the long run. To that end, the authors further highlight an observation by Atchley (1956):

The established method of reporting farmer’s share and [price] spread as a percentage of the consumer’s food dollar has contributed to a wide misunderstanding of the true economic relation of agriculture to food processing and distribution. It has made them appear as competitors for a fixed value, rather than as partners in the production of greater value.

With all that in mind, here’s the rub. The “broken market” pundits draw attention to the difference between farmers’ share at the near-term peak in 2015 - and the subsequent plunge during Covid. But that’s cherry picking two extremes to make their case. Amidst the realities of the business, it’s especially important to take a long, broad view rather than leveraging a single economic measure towards policy - especially if that measure’s usefulness is questionable to begin with.

Nevil Speer is an independent consultant based in Bowling Green, KY. The views and opinions expressed herein do not reflect, nor are associated with in any manner, any client or business relationship. He can be reached at nevil.speer@turkeytrack.biz.