Market Highlights: International Beef Trade Matters

By: Andrew P. Griffith, University of Tennessee

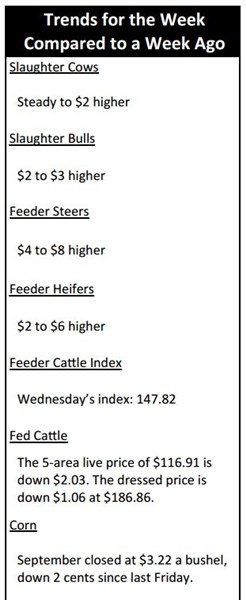

FED CATTLE: Fed cattle trade was not well established at press. Asking prices on a live basis ranged from $120 to $122 while bids were mainly $118. Asking prices on a dressed basis were $190 to $192. The 5-area weighted average prices thru Thursday were $116.91 live, down $2.03 from last week and $186.86 dressed, down $1.16 from a week ago. A year ago prices were $152.73 live and $239.29 dressed.

As has been the case in most weeks the past few years, significant cash cattle trade did not occur until late on Friday. With so much uncertainty, neither the cattle feeder nor the packer is willing to budge on price negotiations until the last second. It almost seems now that folks in the futures market do not want to make trades until they know what happened in the cash market.

The price actions and reactions the market has witnessed the past several months is more due to speculative and technical uncertainty than fundamental supply and demand estimations and expectations. The market will eventually clean itself up, but it may take down several people while doing it.

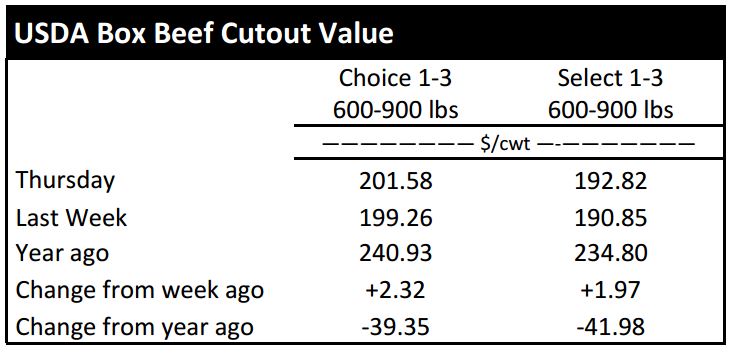

BEEF CUTOUT: At midday Friday, the Choice cutout was $201.51 down $0.07 from Thursday and up $2.56 from last Friday. The Select cutout was $193.51 up $0.69 from Thursday and up $3.06 from last Friday. The Choice Select spread was $8.00 compared to $8.50 a week ago.

Packers did not experience huge gains this week from increases in wholesale beef prices, but a positive price movement is welcome. Purchases for Labor Day featuring have yet to hit full stride, but they are sure to pick up the next couple of weeks.

It is not only the domestic market that is important, but the international market is a big player. Through the first six months of the year, beef and veal imports are 13.0 percent lower than the same time period one year ago.

Australia and New Zealand are the two largest imports sources, but 2016 beef imports through the first half of the year from Australia and New Zealand are down 30.6 and 6.8 percent respectively compared to the same months in 2015. Brazil and Uruguay are both down more than 29 percent while Canada and Mexico are both up more than 11 percent.

Exports for 2016 through June are 2.0 percent higher than 2015 exports through the first six months of the year. Exports to Japan, Mexico, and South Korea are 8.8, 6.4, and 17.4 percent higher respectively compared to the same months one year ago.

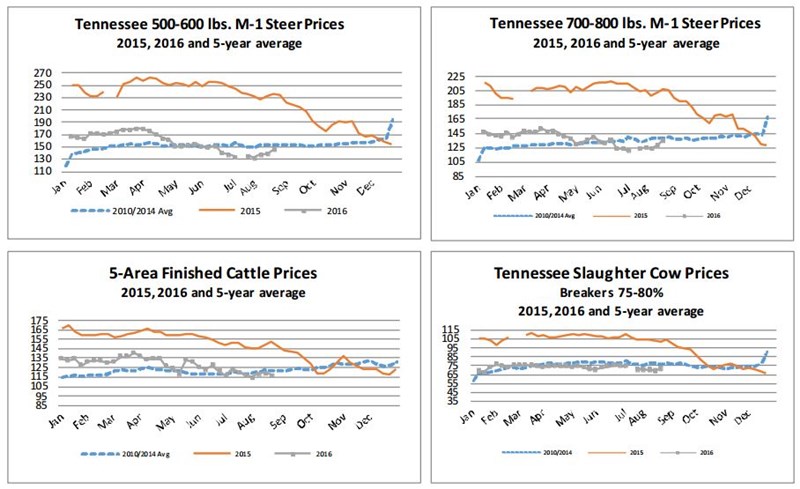

OUTLOOK: It was another positive week for cattle prices as feeder cattle futures were firmer which resulted in stronger cash prices. Based on Tennessee weekly auction averages, steer prices were $4 to $8 higher than last week while heifer prices were $2 to $6 higher.

Feeder cattle prices generally experience seasonal strength in August and that is exactly what has happened the first two weeks of the month. It may be tough for prices to continue escalating as they have the past two weeks, but seasonal strength is expected to persist at least through the first week or two of September. The strength in feeder cattle prices has helped support calf prices.

Cattle feeders make decisions largely based on the animal that is expected to be the most profitable in relation to gender and weight class of cattle while also evaluating feed costs. The stronger demand for feeder cattle and the higher price has thus supported lighter weight cattle prices as folks look to secure inventory.

Another aspect of the industry supporting feeder cattle prices is the expectation of low corn prices at harvest. Many farmer-feeders are looking for cattle to feed cheap corn. When grain prices are low, farmer-feeders have an incentive to take a risk with cattle as it may be more profitable to walk the corn to market through cattle as opposed to trucking grain.

Producers marketing cattle this fall should be cautious with price expectations. The market has some support in the current time period, but cattle prices generally decline in October and November. It appears prices are setting themselves up for a decline when the spring born calves start coming to market.

Slaughter bull and cow prices showed some signs of life this week. The support from this standpoint is the need for lean grinding beef. This time last year, the U.S. was importing large amounts of lean grinding beef from Australia, but that is no longer occurring since Australian beef producers are attempting to rebuild herds. The slaughter cow market may be tested in the next couple of months, but reduced imports will support prices to some degree.

ASK ANDREW, TN THINK TANK: I have received several emails from industry participants the past few weeks. At first, these emails seemed unrelated, but some comments deserve a second look. These emails discussed cattle feeders in some areas continuing to feed cattle to excessive weights with contracts containing no discounts, calf and feeder cattle prices with little to no price difference based on weight, questions concerning why we continue to import beef when prices are declining, and the disconnect between futures markets and cash markets. It is evident industry participants believe information flow is inadequate to help the cattle and beef industries operate at the desired efficiency. Several information problems that could be occurring include: 1) lack of publically available information, 2) failure to evaluate all available information, 3) misinterpretation of available information, and 4) incomplete publically available information. There may be other shortcomings, but the one sure thing is that industry participants deserve complete information. These problems cannot be addressed overnight, but there has to be a starting point.

Please send questions and comments to agriff14@utk.edu or send a letter to Andrew P. Griffith, University of Tennessee, 314B Morgan Hall, 2621 Morgan Circle, Knoxville, TN 37996.

FRIDAY’S FUTURES MARKET CLOSING PRICES: Friday’s closing prices were as follows: Live/fed cattle –August $116.33 0.30; October $114.53 -0.03; December $115.05 -0.25; Feeder cattle - August $149.08 0.35; September $147.55 0.58; October $144.25 0.20; November $141.25 -0.18; September corn closed at $3.22 up $0.01 from Thursday.