CAB Insider: Does the Other Shoe Drop for Beef Prices?

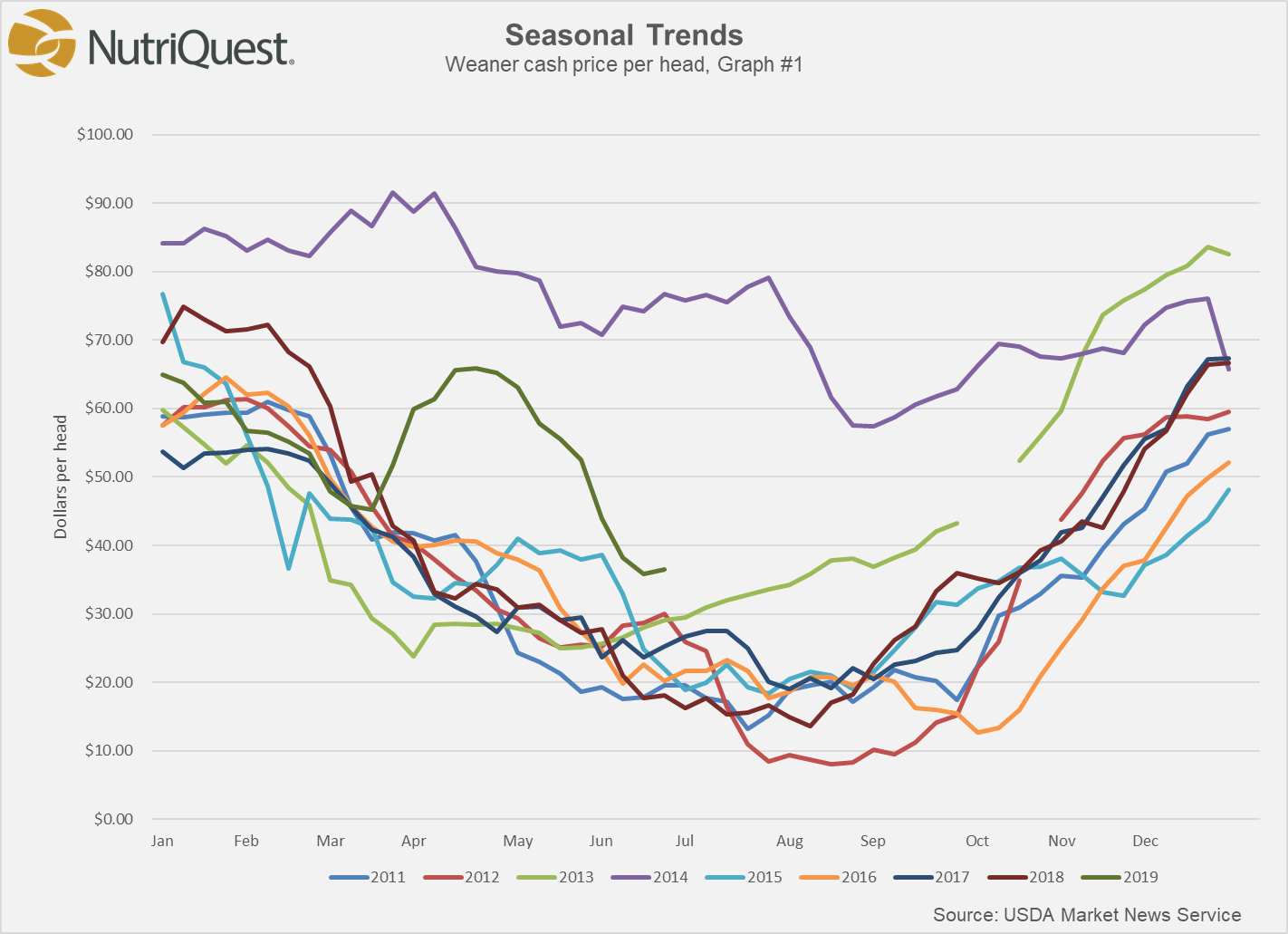

Recent 5-year average price patterns for the benchmark Choice, 600- to 900-lb. carcasses typified from January to March and again from early April to May are more robust while taking the market to the annual highs through additive moves. Meanwhile, the early October to mid-November rally is the only highlight, from a cattle supplier perspective, of any magnitude in the second half of the year. Relying on the 5-year trend alone, we would conclude that the fourth-quarter rally has already been achieved. That’s based on a 5% expected increase from the first week in October to early November.

Predicting an abrupt end to the uptick may be premature this year, however, as demand and exports have been exceptional, given the small fed-cattle product increase, coupled with an early and aggressive buy on holiday roasts from the retail side. While the calendar just turns to November mid-week, only a matter of days separate us from many retail protein buyers turning their eyes away from beef in favor of turkeys. At least steady demand through November is a decent bet but the corresponding 5% anticipated decline in cutout values into December lies in wait. Last week’s Certified Angus Beef (CAB) brand cutout value was $7.05/cwt. above the latest weekly Choice value.

Market Update

After six straight weeks stuck at $111/cwt., the fed cattle market finally broke out to average $114/cwt. last week. Four factors contributed to the higher market.

First, Live Cattle futures on the Chicago Mercantile Exchange moved higher with the December contract trading up to $118/cwt. before a lower close Friday, emboldening cattle-feeder thinking that they should be pricing their inventory higher.

Second, there has been a fair amount of moisture across a large enough share of the cattle feeding region to pull down carcass weights and negatively impact performance, creating at least a momentary reversal in the fall carcass weight uptrend.

Third, the tighter fed cattle supplies foretold for so many months have arrived now in the fourth quarter, and it appears the industry is fairly current despite the seasonal weight and yield-grade issues that created some backlog in Iowa and eastern Nebraska.

Fourth, packers remain very profitable and can afford to pay a few more dollars for cattle to secure inventory, especially as the spot market cutout values increased last week. Year-on-year comparisons for carcass quality grades will be difficult to track now and the next few weeks because a year ago, USDA made adjustments to the camera grading lines due to hardware upgrades dating back more than a year and a half. The 12-week average for CAB acceptance rests at 33.9%, compared to 32.3% for that period last year.

The Certified Angus Beef brand carcass cutout increased last week by $3.60/cwt. with stronger prices across most of the carcass. The rib continues to lead the way with wholesale pricing well ahead of a year ago at a margin of $1.07/lb. over the same week last year on the lip-on, heavy ribeyes. The question surrounding that item is whether this early exuberance will be sustained all the way to mid-December.

Cooler fall weather has end-meats for roasts a feature at the retail level. There were also stronger prices, particularly on the round items last week, placing the round in the second position for primal price inflation. Strip loins struggled to get any further price traction and remain at a subdued price, yet gains on top butts, tenderloins and loin thin-meats carried the total loin market higher.

Briskets in the spot market are also capturing a bit of an unseasonal demand surge in the past couple of weeks with a current price of $2.71/lb. Items from the chuck saw mixed values with clods, flat irons and clod tenders trading a bit cheaper but the remaining items pricing slightly higher.

Heifers Factor Into Prime Grade Uptrend

We must take a big step back from the details of beef market and production trend data once in a while to gain perspective. Currently, that distant view shows one of the largest changes in 2018 is the % of fed steer and heifer carcasses reaching the Prime quality grade, touching a record 8.9% the second week of October, adding to an already impressive 33% increase in Prime tonnage so far this year.

We’ve covered it in detail in the Insider recently so let’s cut to the chase for this week’s focus. It’s well-known in academic, cattle-feeding and packing circles that heifers achieve higher marbling scores than steers at a similar endpoint of backfat thickness. Therefore a larger proportion of heifers in the fed-cattle harvest increases average quality grade across the fed cattle supply chain.

As well, calendar