While the heifer percentage in feedlots remains above the average of the past ten years, the decline from January to April is an encouraging sign that heifer feeding is perhaps slowing.

In a steady market, fed prices would typically peak seasonally about now and move lower through the third quarter before increasing to year end, but there is good reason to expect the uptrend will continue in 2023.

Given growing expectations that drought conditions will moderate through the coming months, bred cow and heifer values are likely to increase sharply by this fall.

Over the past four weeks beef production has averaged 6.4% lower than last year. Production is expected to drop more sharply the remainder of the year.

Feedlot inventories are at their lowest point in 29 months and placements have been lower in 10 of the past 12 months. Here's what historical data shows about how the trend may evolve in the coming months.

Despite record beef exports in 2022, signs of weakening beef trade were developing late in the year with beef exports down year-over-year in both November and December.

With continuing drought, it is not clear exactly how cattle and beef market timing will develop going forward, but the question is not one of whether beef production will fall, but rather how fast and how much in 2023.

Uncertain when, but there will be strong interest in rebuilding the herd when conditions permit. Leaving aside the question of more drought, what's possible in 2023 given current availability of replacement heifers?

Although some recent moisture has reduced drought in Oklahoma, over 80 percent of the state remains in some stage of drought. Cattle producers face considerable challenges to maintain herds through winter.

Feedlots inventories should continue to tighten, and cattle slaughter should decline in the coming weeks, although continued drought conditions may slow the rate of decrease if more animals are liquidated.

Oklahoma has been impacted by drought more than any other state, by several measures. The January 1, 2023, inventory of all cattle and calves in Oklahoma was down 11.5 percent.

With the opportunity to visit a number of cattle feeding operations and learn a bit about how cattle feeding works in this unique environment, Dr. Derrell Peel of OSU shares his experience from his recent trip to Canada.

The new year looks to contrast with last year with noticeably tighter cattle numbers, especially at the feedlot level, driven by previous herd liquidation and sharply lower feeder cattle supplies.

Drought pushed more cattle into feedlots earlier this year and kept feedlot totals higher for longer, but the latest on feed data shows numbers declining.

In general, feeder cattle markets are finishing 2022 strong with momentum going into the new year, even as the drought caused significant changes in the timing of feeder cattle marketing.

Global beef production is forecast to decrease slightly in 2023 and changes in production and consumption will impact global beef exports and imports in the coming year.

Improving feeder futures prices, a stronger fed cattle market and limited supplies of feeder cattle all combined to push prices higher following Thanksgiving.

The combination of effects from the pandemic in 2020 and drought since 2020 has pushed the peak in feedlot numbers and cattle slaughter into 2022, well past the cyclical peak in the calf crop in 2018.

The volume of feeder cattle sold in Oklahoma increased nearly 20% from mid-July to mid-October as a result of the drought. Since then, volumes have been down and likely smaller through November.

USDA reported the first year-over-year decrease in feedlot inventories since December 2021, but the decline came from steer numbers as heifers on feed were up 1.4%.

In recent years, Mexican beef production has continued to grow while total domestic consumption has been relatively stable leading to growing beef exports from the country.

The drought situation in Oklahoma is increasingly critical with winter approaching. USDA rated Oklahoma pasture conditions 72 percent poor to very poor in the latest crop progress report.

As much as 11 percent of Oklahoma's winter wheat has been planted despite soil moisture profiles that are bleak at best. Wheat grazing prospects look dim and risky this fall.

The integration of beef and cattle markets in North America includes trade in live cattle between Canada, Mexico, and the U.S. The recent trade data provides an update of activity for the first seven months of this year.

Calf prices typically reach a seasonal low around October. This year, however, calf prices have moved counter-seasonally higher this summer as part of a general trend of tighter supplies and higher prices.

Given the limited hay supply, proportionally more wheat pasture is likely to be used for cow herds than for stockers. Even if there is wheat pasture, stocker demand may be somewhat lighter than usual this year.

Aided and abetted by drought, feedlots put together another month of large placements in July despite growing indications that feeder supplies are declining.

Amid continuing drought, the 2022 hay supply data illustrate why so much herd liquidation has occurred this year. It also speaks to the continuing challenges that cattle producers will face to get through the winter.

Beef exports in June 15.2% higher while beef imports were down 15.3%. Strong exports are helping offset domestic demand struggles as beef imports decreased in the face of higher cow slaughter and lean beef production.

Drought impacts have accelerated sharply in the southern plains in July, with the volume of feeder cattle in Oklahoma auctions up 24% the last two weeks and the volume of cows and bulls up nearly 124%.

Lower cattle inventories combined with a cattle on feed inventory about equal to last year, is expected to lead to a roughly three percent decrease year over year in estimated feeder supplies outside of feedlots.

None of the smaller beef export markets account for more than 1.5% of the total, but many small markets are growing and contributing to a more robust set of export markets for U.S. beef.

Exactly how continuing drought, reduced forage production and high feed prices will impact cattle and beef markets in the coming months remains uncertain.

It will take much of the remainder of the year for feedlots to work through the current inventory and we can’t be sure what additional impacts the drought may have in the coming months.

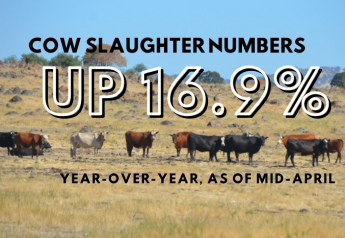

Through May, beef cow slaughter for the year-to-date is 15% higher. While some drought reduction has improved pasture conditions, range and pasture conditions remain at the worst level ever for this time of year.

As we move into June, cattle markets are transitioning into summer mode, reflecting seasonality and a myriad of other factors which are currently impacting markets.

Global beef trade is projected to continue expanding to new record levels in 2022. The top four beef exporting countries represent about 60 percent of the 2022 projected global total in the USDA report.

Spring green-up has been muted by the ongoing drought and each passing week is critical and by any measure, the U.S. is in the worst condition now of any May in at least the last 35 years.

The ongoing drought continues to squeeze available hay supplies and drought this year is a severe threat to 2022 hay production. May 1 hay stocks in the 17 plains and western states were down 17.7 percent year-over-year.

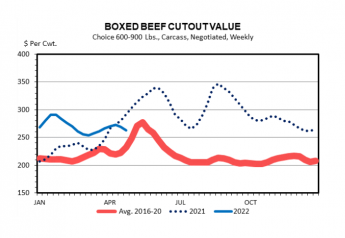

Boxed beef prices have come down from a period of extremely strong demand and adjusted down from a counter-seasonal January peak to current levels, 11.2 percent lower compared to the last week of January.

The fast pace of cow slaughter thus far implies the likelihood of significant beef cow herd liquidation in 2022. The next few months will likely have impacts on the cattle industry for several years.